In today’s world, personal financial planning has become an essential aspect of life. It is crucial to have a plan in place to secure your financial future and achieve your long-term goals.

In this article, we will discuss the importance of personal financial planning and its benefits. We will also provide you with step-by-step guidance on creating a personal financial plan and share some tips for successful financial planning.

By following these guidelines, you can take control of your finances and pave the way for a brighter financial future.

Table of Contents

Definition of Personal Financial Planning

Personal financial planning is managing your money to achieve your financial goals. It involves creating a budget, saving for emergencies and future expenses, investing wisely, and managing debt. The goal of personal financial planning is to ensure that you have enough money to live comfortably now and in the future.

The goal of personal finance planning is to ensure that you have enough money to live comfortably now and in the future.

workandhometips.com

Many people avoid financial planning because they think it’s complicated or time-consuming. However, taking the time to create a personal financial plan can help you make better financial decisions, reduce stress, and achieve your long-term goals.

In this comprehensive guide, we will explore the benefits of personal financial planning, the steps involved in creating a personal financial plan, and tips for successful financial planning. Whether you’re just starting out or looking to improve your current financial situation, this guide will provide you with the tools and knowledge you need to take control of your finances and achieve your goals.

Read on to see how personal financial planning can benefit you.

4 Benefits of Personal Financial Planning

1. It helps you achieve your financial goals

Personal financial planning is an essential aspect of life that can bring numerous benefits. One of the most significant benefits of personal financial planning is that it helps you to achieve your financial goals.

By creating a plan, you can identify your short-term and long-term financial objectives and work towards achieving them systematically. You avoid missing out on the essential things you need to work on and leave out the unimportant ones.

2. Helps you manage your finances effectively

Another benefit of personal financial planning is that it helps you to manage your finances effectively. With a plan in place, you can track your income and expenses, monitor your savings, and make informed decisions about investments and debt management. This can help you to avoid overspending, reduce debt, and build wealth over time.

Many people find themselves in the quagmire of unpaid debts. With financial planning, this situation can be avoided. Without a good financial plan, you won’t be able to manage your finances effectively.

3. Gives you a peace of mind

Personal financial planning can also provide you with peace of mind. Knowing that you have a solid financial plan in place can ease stress and anxiety related to money matters. It can also help you prepare for unexpected events, such as job loss, illness, or other emergencies.

These are the realities of life thus must always be incorporated in one’s personal strategies to overcome the challenges associated with this imperfect life we face. We realize that we do not have total control over our life and what happens to us. But with good personal financial planning, job loss, illness that are unavoidable, and unforeseen emergencies can be addressed much better than without any plan at all.

Relieved of the stress associated with unpredictable events, an excellent plan would undoubtedly give you a peace of mind that you will cherish. It makes you more happy.

4. Improves your overall quality of life

Besides these benefits, personal financial planning can also help you improve your overall quality of life. By managing your finances effectively, you can free up more time and resources to pursue your passions, travel, spend time with loved ones, or engage in other activities that bring you joy.

Overall, personal financial planning is a crucial component of achieving financial stability and success. By taking the time to create a comprehensive plan and following through with it, you can reap the many benefits that come with effective financial management.

Your life gets better, and you become healthier thus being able to do more and earn more.

6 Essential Steps in Creating a Personal Financial Plan

Creating a personal financial plan can seem overwhelming, but breaking it down into manageable steps can make the process much easier. Here are some key steps to follow:

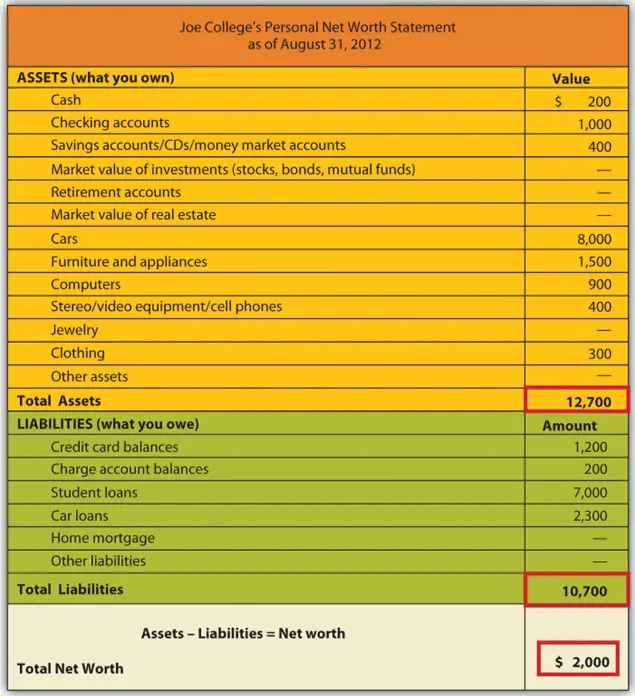

Step 1: Assess your current financial situation

Before you can create a plan, you need to know where you stand financially. This includes taking stock of your income, expenses, debts, and assets. Below is an example balance sheet showing Joe’s assets and liabilities to illustrate this step.

This example shows a realistic assessment of Joe’s financial situation where planning can take off.

Step 2. Define your financial goals

What do you want to achieve with your money? Whether it’s saving for retirement, buying a house, or paying off debt, having specific goals in mind will help guide your financial decisions.

Avoid making vague goals like “become rich” or “I want to make more money.” Set specific targets like a six-month salary savings, a Lamborgini “Huracàn”, or anything like that.

Step 3. Develop a budget

A budget is a crucial tool for managing your money and achieving your goals. It helps you track your expenses and ensure that you’re living within your means.

That last statement is very important. You should not spend more than you earn. If you want to spend more, earn more. Have several sources of passive income.

Step 4. Create a savings plan

Create a savings plan: Saving money is essential for achieving long-term financial goals. Determine how much you need to save each month to reach your goals and set up automatic transfers to make it.

Make sure that the amount of savings you set aside is practically feasible. This should be the amount left after all necessary payment obligations are met or the essentials for good health and basic essentials are met.

Step 5. Manage your debt

If you have debt, it’s important to have a plan for paying it off. Consider strategies like the debt snowball or avalanche method to tackle your debts strategically. Whichever method you choose, just do the payments consistently.

If you have a windfall, or a substantial amount of money from an unexpected source, pay off all your debts at once. It is better to be free of debt than spend money on your wants that will keep you within the shackles of never-ending anxiety and stress.

Step 6. Protect yourself and your assets

Insurance is an important part of any financial plan. Make sure you have adequate coverage for your health, home, car, and other valuable assets. Find one that you can practically afford.

By following these steps, you can create a comprehensive personal financial plan that will help you achieve your goals and secure your financial future.

4 Tips for Successful Personal Financial Planning

When it comes to personal financial planning, there are a few tips that can help ensure success. I share four tips for successful personal financial planning in the next paragraphs.

1. Set realistic goals

Foremost, it’s important to set realistic goals. This means taking into account your current income, expenses, and debt, as well as any future plans or aspirations you may have. Once you’ve established your goals, create a plan that outlines the steps you’ll need to take in order to achieve them.

2. Track your spending

Another key tip for successful personal financial planning is to track your spending. This means keeping a detailed record of all your expenses, from rent and utilities to groceries and entertainment. By doing so, you’ll be able to identify areas where you may be overspending and make adjustments accordingly.

There are many personal financial apps available for your use. Choose one that meet your needs.

3. Establish an emergency fund

It’s also important to establish an emergency fund. This should be a separate savings account you contribute to regularly and only use in the event of an unexpected expense or loss of income.

Experts recommend having at least three to six months’ worth of living expenses saved up in your emergency fund although Miller says it should be at least one year given the uncertainty of employment in recent times.

4. Review and adjust your financial plan

Finally, don’t forget to regularly review and adjust your financial plan as needed. Life circumstances can change quickly, and your financial goals and priorities may shift over time. By staying flexible and adaptable, you’ll be better equipped to achieve long-term financial success.

God speed to your successful application of these tips.